Blockchain technology is a revolutionary way to store and share data. At its core, it is a decentralized digital ledger that records transactions across many computers. The data is stored in blocks, which are then linked together in a chain. This structure makes the data highly secure, transparent, and resistant to tampering. You can learn more about blockchain here, on the page dedicated to exploring its uses and applications.

One of the key elements that sets blockchain apart is that once a transaction is recorded, it cannot be altered. This immutable nature ensures the authenticity and integrity of the data, making it ideal for industries where trust is paramount. Understanding blockchain is important, especially for those looking to pursue careers in emerging tech fields. Although blockchain is often associated with cryptocurrencies like Bitcoin, its potential applications extend far beyond digital currencies.

How Blockchain Works

To understand how blockchain works, think of it as a digital book shared among a network of computers. Every time a transaction takes place, it’s recorded in this book as a block of data. These blocks are then linked to previous blocks, forming a chain of transactions.

Each block contains three essential parts: the data, a hash (a unique identifier for the block), and the hash of the previous block. This creates a system where every block is connected and dependent on the one before it, making the data incredibly secure.

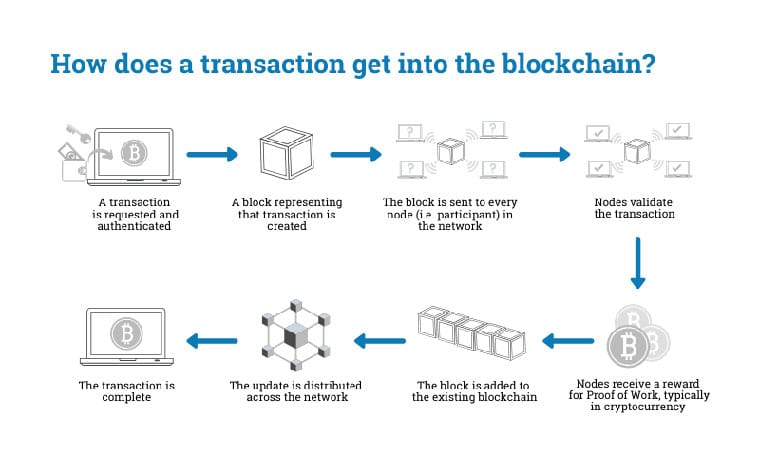

Here’s a step-by-step breakdown of how blockchain transactions work:

1. A transaction is requested.

2. The transaction is broadcast to a network of computers (nodes).

3. The nodes validate the transaction.

4. Once verified, the transaction is added to a block of data.

5. The block is added to the existing chain, securing the data.

6. The transaction is complete, and the blockchain is updated across all nodes.

Key Features of Blockchain Technology

Blockchain stands out due to several unique features that make it a game-changer across various industries:

- Decentralization: Blockchain operates without a central authority. Instead, data is distributed across a network, increasing security and reducing risks of data breaches.

- Transparency: Every participant in the network has access to the same data, ensuring trust and accountability.

- Immutability: Once data is recorded on the blockchain, it cannot be changed or deleted.

- Security: Blockchain uses advanced cryptography to secure data, making it resistant to hacks.

Decentralization

One of the key aspects of blockchain technology is decentralization. Unlike traditional systems where a central authority (like a bank or government) controls data, blockchain distributes data across a network of nodes. This distribution ensures that no single entity has control over the entire system, making it more secure and less prone to failure.

Decentralization also enhances trust, as participants in the network do not need to rely on a central authority. Instead, they rely on the consensus of the network to validate transactions.

Transparency and Security

Blockchain’s transparency is another vital feature. Since the data is shared among all participants, everyone in the network can see the same information. This transparency fosters trust between users.

Security is ensured through cryptography. Each block contains a unique code (hash), and any attempt to alter the data would require changing the hash of that block and all subsequent blocks. This process is computationally infeasible, making blockchain highly secure.

Types of Blockchain Networks

Blockchain technology can be implemented in various ways, depending on the needs of the network. The four main types of blockchain networks are:

- Public Blockchain: Anyone can join and participate in a public blockchain network. It’s entirely decentralized, making it the most transparent type of blockchain.

- Private Blockchain: A private blockchain is permissioned, meaning only authorized users can access it. It is often used by organizations that need a controlled environment.

- Consortium Blockchain: In a consortium blockchain, several organizations collaborate to manage the network, balancing decentralization and control.

- Hybrid Blockchain: Hybrid blockchains combine elements of both public and private blockchains, allowing certain data to be public while keeping other parts private.

Public vs. Private Blockchain

Public and private blockchains serve different purposes. Public blockchains, like Bitcoin and Ethereum, are open to anyone and provide the highest level of transparency. They are ideal for decentralized applications where trust needs to be established without a central authority.

On the other hand, private blockchains are restricted to a specific group of users. While they offer more control and privacy, they may lack the full benefits of decentralization. These are often used in enterprise settings where control over data is crucial.

Applications of Blockchain Technology Across Industries

Blockchain’s versatility has made it a valuable tool across multiple industries. Some of the most notable applications include:

- Finance: Blockchain enables faster, cheaper, and more secure transactions, making it ideal for financial services.

- Healthcare: Blockchain improves data sharing between healthcare providers, ensuring patient records are accurate and secure.

- Supply Chain Management: Blockchain enhances transparency and traceability in supply chains, ensuring product authenticity.

- Real Estate: Blockchain simplifies property transactions by enabling smart contracts, reducing the need for intermediaries.

Blockchain in Finance

In the financial sector, blockchain has introduced significant changes through cryptocurrencies like Bitcoin and Ethereum. It enables secure peer-to-peer transactions without the need for intermediaries such as banks. Moreover, decentralized finance (DeFi) is emerging as a new way to provide financial services, allowing users to lend, borrow, and trade without traditional financial institutions.

Smart contracts are another innovation in finance, automating agreements based on predefined conditions. This automation reduces transaction costs and speeds up processes.

Blockchain in Supply Chain Management

Blockchain technology plays a pivotal role in supply chain management. By using a shared ledger, companies can track products from the point of origin to the final destination, improving transparency and reducing fraud. Consumers can verify the authenticity of products, such as food or luxury items, ensuring they receive what they paid for.

Benefits and Challenges of Blockchain Technology

While blockchain offers numerous benefits, it also faces several challenges that must be addressed for widespread adoption.

Benefits of Blockchain

- Enhanced Security: Data stored on a blockchain is encrypted and tamper-proof, providing an extra layer of security.

- Cost Efficiency: By eliminating intermediaries, blockchain reduces transaction costs and speeds up processes.

- Faster Transactions: Blockchain transactions can be processed in minutes, compared to days in traditional banking systems.

Challenges of Blockchain

- Energy Consumption: Blockchain, especially public networks, requires significant computational power, leading to high energy consumption.

- Regulatory Issues: Governments are still figuring out how to regulate blockchain, which can create legal uncertainties.

- Scalability: As blockchain networks grow, they face challenges in scaling efficiently to handle more transactions.

Future Trends in Blockchain Technology

Blockchain is still evolving, and several trends are expected to shape its future. Interoperability between different blockchain networks is becoming a priority, allowing for better communication and collaboration. Environmental concerns are pushing for more energy-efficient consensus mechanisms, such as Proof of Stake (PoS).

Additionally, as blockchain technology matures, mainstream adoption across industries like healthcare, finance, and government is expected to rise. The integration of blockchain with other technologies, such as artificial intelligence (AI) and the Internet of Things (IoT), will further expand its capabilities.

Final Thoughts on Blockchain Technology

Blockchain technology has transformed how data is stored, shared, and secured. Its decentralized nature, transparency, and immutability make it a powerful tool across industries. While challenges like scalability and energy consumption remain, the future of blockchain looks promising, with ongoing innovations likely to address these issues. As blockchain continues to evolve, its potential to reshape industries is vast, making it one of the most exciting technologies to watch in the coming years.

1 Comment

Leave a Reply

Blockchain technology is truly revolutionary, offering a decentralized way to store and manage data with unparalleled transparency and security. It’s fascinating how it’s being applied across industries like finance, healthcare, and supply chain management. For anyone looking to explore blockchain in simpler terms and understand its potential for reshaping the future, this guide is a great start!